HDB Financial Services, an NBFC and subsidiary of HDFC Bank, is making its market debut with its long-awaited IPO. As one of the leading consumer finance companies in India, HDB Financial has built a strong franchise over the years. However, its IPO has sparked debate due to the pricing discrepancy between its unlisted and listed valuations and mixed signals about its growth prospects.

This article provides an in-depth look at HDB Financial Services’ IPO - its business model, financial performance, and key risks - to help you assess if it deserves a place in your portfolio.

Table of Contents

- Understanding HDB Financial Services & Its IPO

- HDB Financial Services Business Model: A Retail-Focused NBFC

- Market Position & Clientele: Pan-India Reach

- Industry Outlook: The Growth of NBFCs in India

- Financial Performance: Profitability, Growth, and Challenges

- HDB Financial Services IPO Details: Price, Dates, and Allocation

- Investment Strengths: Why HDB Financial Services Stands Out

- Potential Risks: What Investors Must Consider

- Strategic Vision: The Roadmap for HDB Financial Services

- Competitive Landscape: HDB vs Other NBFCs

- Final Investment Conclusion: Is HDB Financial Services IPO Worth Considering?

- FAQs

HDB Financial Services Limited, incorporated in 2007, operates as a retail-focused Non-Banking Financial Company (NBFC). Its parent entity, HDFC Bank, has established HDB Financial as a trusted brand with a wide presence across India. HDB Financial Services is set to launch its IPO from 25 June 2025 to 27 June 2025, with a tentative listing date of 2 July 2025. The IPO comprises a fresh issue of Rs 2,500 Crore and an offer for sale of Rs 10,000 Crore, totalling Rs 12,500 Crore.

/content-assets/848a5c529cfa41e2b564eb7e15a92708.png)

Wrap-Up: HDB Financial Services’ IPO aims to raise significant capital to expand its loan book and support its parent company’s long-term growth.

HDB Financial Services operates across three core segments:

-

Enterprise Lending - Enterprise Lending is HDB’s largest business segment, contributing approximately 40.8% to its Assets Under Management (AUM) in FY24. It involves providing both secured and unsecured loans to Micro, Small, and Medium Enterprises (MSMEs) for purposes such as business expansion, working capital needs, and equipment purchases.

-

Asset Finance - Contributing around 37.9% to FY24 AUM, Asset Finance includes loans for purchasing new and used commercial vehicles, construction equipment, and tractors. This segment primarily serves self-employed individuals and small businesses operating in transport, construction, and agriculture.

-

Consumer Finance - This segment accounted for 21.3% of AUM in FY24 and includes products like personal loans, two-wheeler loans, and consumer durable loans. Targeted at both salaried and self-employed individuals, it supports personal consumption and lifestyle needs.

Wrap-Up: HDB Financial Services’ diversified loan offerings and deep-rooted distribution channels make it a strong player in the retail NBFC space.

Want to compare HDB Financial's business model with other upcoming IPOs? Check out Sambhv Steel Tubes IPO Analysis & Growth Potential to see how growth prospects play out in different industries.

HDB Financial operates across 1,772 branches (as of Sep 2024) in 1,162 towns and cities across 31 States and Union Territories. Notably, over 80% of its branches are located outside India’s top 20 cities, making it one of the best-positioned NBFCs for rural and semi-urban expansion.

Wrap-Up: HDB Financial Services’ deep rural and semi-urban penetration provides access to under-banked markets, making it pivotal in India’s financial inclusion story.

The NBFC (Non-Banking Financial Company) sector in India is on a strong growth path due to several favourable factors:

- High Demand for Credit: With growing aspirations and needs, more individuals and small businesses are borrowing for homes, vehicles, education, business expansion, etc. NBFCs play a crucial role in meeting this demand, especially in areas underserved by traditional banks.

- Improved Financial Awareness: People now better understand how loans work, including EMIs, credit scores, and interest rates. This increasing financial literacy encourages more people to approach formal lenders like NBFCs.

- Supportive Policies and Digital Adoption: Government initiatives and regulatory support from RBI have strengthened the NBFC sector. At the same time, digital technologies like online KYC, mobile apps, and AI-based credit scoring have made lending faster, easier, and more efficient.

With these growth drivers, HDB Financial Services is well-positioned to benefit, thanks to its wide product range and strong presence in growing markets.

Interested in other IPOs with strong financial potential? Check the ongoing HDB Financial Services IPO for the latest updates and detailed metrics.

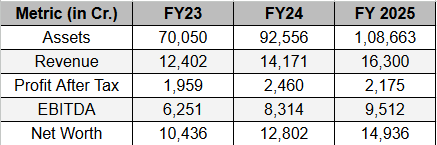

HDB Financial Services has demonstrated robust growth across its financial metrics:

Although revenue increased by 14% from FY24 to FY25, Profit After Tax declined by 12%, due to rising non-performing assets and higher credit costs. However, the consistent growth in EBITDA and Net Worth reflects strong operational efficiency and long-term financial stability.

Key Financial Ratios (FY25)

|

Ratio

|

Value (FY25)

|

|

EBITDA Margin

|

58.4%

|

|

Net Profit Margin

|

13.3%

|

|

Return on Equity (ROE)

|

14.7%

|

|

Return on Assets (ROA)

|

2.16%

|

|

Net Non-Performing Assets

|

0.99%

|

|

Debt-to-Equity Ratio (D/E)

|

5.85x

|

Insights on Key Metrics

- EBITDA margin improved YoY, from 58.36% in FY24 to 58.67% in FY25, reflecting stronger operational control and improved cost efficiency. This is a positive indicator, especially for an NBFC serving semi-urban and rural markets where operating costs are often higher.

- Despite revenue growth, Net Profit fell 11.6% YoY to 2460.84Cr. in FY25 from 2174.92 Cr. in FY24. This drop is attributed to increased credit costs and Non-performing assets.

- Return on Assets also declined from 3.03% in FY24 to 2.16% in FY25. It indicates a more modest return on total assets, which is expected in NBFCs with high leverage. The decline again points to pressure on net profitability.

- Its Debt-to-Equity Ratio increased to 5.85x in FY25 from 5.81x in FY24. This much leverage shows HDB is funding growth aggressively through borrowings. While typical for NBFCs, it raises the importance of maintaining strong asset quality and prudent risk controls.

Wrap-Up: HDB Financial Services shows strong growth metrics despite a temporary drop in PAT, suggesting resilient operational performance and long-term potential.

|

Details

|

Information

|

|

Issue Date

|

25–27 June 2025

|

|

Issue Type

|

Book Building IPO

|

|

Fresh Issue

|

3.38 Crore Shares (₹2,500 Crore)

|

|

Offer for Sale (OFS)

|

13.51 Crore Shares (₹10,000 Crore)

|

|

Price Band

|

₹700–₹740 per share

|

|

Lot Size

|

20 Shares

|

|

Listing Date (Tentative)

|

2 July 2025

|

Investor Category Reservation:

|

Category

|

Shares offered

|

|

QIB

|

44.92%

|

|

NII

|

13.48%

|

|

Retail

|

31.44%

|

|

Employee

|

0.16%

|

|

Shareholder Quota

|

10.00%

|

HDB Financial Services brings a mix of strong fundamentals, strategic backing, and operational excellence, making it a compelling choice for investors. Here's what sets the company apart:

- Strong Parentage – Backed by HDFC Bank

Being a wholly-owned subsidiary of HDFC Bank, one of India’s most trusted and financially sound banks, gives HDB significant advantages:

- Easy access to capital at competitive rates

- Higher trust among customers and stakeholders

- Operational and governance best practices aligned with a reputed parent

- Extensive Rural and Semi-Urban Distribution

HDB has built a wide network across Tier 2, Tier 3 cities and rural India, where access to credit is still limited.

- This network helps it serve underserved markets

- Offers a first-mover advantage in areas with low competition

- Drives inclusive lending and strong customer retention

- Diversified Loan Portfolio

HDB’s loan book is spread across three core verticals:

- Enterprise Lending (MSMEs)

- Asset Finance (vehicles, tractors, construction equipment)

- Consumer Finance (personal and household loans)

This diversification reduces risk and ensures steady revenue flow across economic cycles.

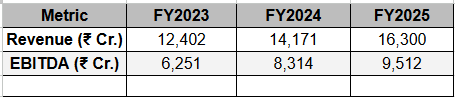

- Consistent Revenue and EBITDA Growth

HDB has shown steady growth, with revenue and EBITDA rising consistently from FY23to FY25.

This indicates strong operational performance and efficient cost management, even during periods of macroeconomic uncertainty.

- Omnichannel Distribution Model

HDB uses a hybrid model combining physical branches and digital platforms, which enhances both reach and efficiency.

- Enables customers to access services easily, whether online or offline

- Reduces turnaround time for loans

- Enhances scalability and cost-effectiveness

While HDB Financial Services shows strong growth potential, investors should also be aware of the following key risks.

- High Debt Leverage

- HDB operated with a debt-to-equity ratio of 5.85x in FY24 and 6.2x in FY25, which is typical for NBFCs but poses a risk if market liquidity tightens or borrowing costs rise.

- High leverage can amplify both gains and losses, increasing financial vulnerability during downturns.

- Dip in Profitability (FY24–FY25)

- While revenue grew by 14%, Profit After Tax declined by 12% in FY25, suggesting possible margin pressures or higher provisioning costs.

- Sustained profit decline could affect investor sentiment and valuation.

- Regulatory Oversight

- NBFCs are under increasing RBI and government scrutiny, especially concerning lending practices, liquidity, and capital adequacy.

- Any tightening in regulations could limit growth or increase compliance costs.

- Rising Competition

- The financial services space is seeing intense competition from other NBFCs, digital lending platforms, and FinTech startups offering quicker and tech-driven solutions.

- This could lead to pricing pressure and customer churn for traditional NBFCs like HDB.

- Economic Cyclicality

- NBFCs are highly sensitive to macroeconomic conditions.

- During periods of slow GDP growth, inflation, or job losses, default rates may rise, especially in the consumer and MSME segments where HDB has a large exposure.

Understanding the risks of HDB Financial Services IPO can be crucial. Learn more about the Crizac Limited IPO Review to make an informed decision about investing in this new market.

The IPO proceeds will help HDB Financial Services:

- Strengthening the Loan Book in Rural and Semi-Urban India

- HDB plans to deepen its presence in underserved and unbanked markets, particularly in Tier 2, Tier 3 cities, and rural regions.

- These areas offer high growth potential as formal credit access remains limited, especially for MSMEs and individual borrowers.

- By expanding its loan book here, HDB can tap into a growing and loyal customer base while supporting financial inclusion.

- Enhancing Digital Offerings and Expanding Distribution

- A major part of the strategy involves investing in digital transformation, including mobile platforms, online loan origination, digital KYC, and AI-based credit assessments.

- This will improve customer experience, reduce operational costs, and make credit delivery faster and more efficient.

- Additionally, HDB will broaden its physical distribution network through new branches, franchise models, and third-party partnerships.

- Maintaining Robust Credit Quality While Scaling

- As it grows, HDB remains committed to managing credit risk carefully by maintaining strict underwriting standards and using advanced data analytics to assess borrower profiles.

- This focus on quality over aggressive volume growth will help safeguard its portfolio and protect long-term profitability.

Wrap-Up: HDB Financial Services aims to consolidate its position as a leading NBFC by leveraging its parentage, deep rural presence, and multi-product offerings.

HDB Financial Services operates in a competitive NBFC space, facing challenges from both traditional players and emerging FinTech lenders. However, its strong HDFC Bank parentage, diversified loan portfolio, and rural/semi-urban focus give it a clear edge in scalability and trust.

Key Competitors:

HDB Financial Services shows stronger asset quality than most of the peers with an NNPA of 0.99%, below the group average. However, its ROE (14.72%) and ROA (2.16%) are lower than most leading NBFCs, reflecting moderate profitability. With a debt-to-equity ratio of 5.81x, higher than peers, it is more aggressively leveraged, suggesting higher funding risk but also potential for growth.

HDB’s balanced approach to MSME, vehicle, and consumer lending makes it resilient and well-positioned amid rising credit demand.

If you're weighing multiple IPOs for investment, you can visit Full IPO Overview for a comprehensive look at all ongoing and upcoming IPO opportunities.

For a more visual walkthrough of the HDB Financial Services IPO and its prospects, check out the in-depth video analysis below. Watch the video to get expert insights that complement your reading.

HDB Financial Services, as an NBFC and HDFC Bank subsidiary, gains crucial operational flexibility. Unlike traditional banks, it operates free from strict SLR/CRR constraints, allowing it to target more profitable lending segments. This structural advantage is pivotal to understanding its long-term growth potential.

However, the IPO is in stark contrast with pre-IPO unlisted valuations. Many unlisted investors face losses as the IPO price significantly undercuts earlier trading levels. This highlights the speculative nature and lack of regulation in the unlisted market.

Final Advice: The IPO price reflects a more realistic valuation as compared with its peers. Potential investors are advised to observe the company’s performance post-listing, allowing the market to determine its true worth. Avoid making hasty investments in unregulated markets due to their higher risk and inflated expectations.

Q1: What is the HDB Financial Services IPO?

The HDB Financial Services IPO is a book-built issue aiming to raise Rs 12,500 Crore. It comprises a fresh issue of 3.38 Crore shares and an offer for sale of 13.51 Crore shares. The IPO will be listed on the BSE and NSE.

Q2: When does the HDB Financial Services IPO open and close?

The IPO opens on Wednesday, 25 June 2025, and closes on Friday, 27 June 2025. Allotment is expected to be finalised on Monday, 30 June 2025.

Q3: What is the price band and lot size for the IPO?

The price band is Rs 700–Rs 740 per share. The lot size is 20 shares, making the minimum retail investment Rs 14,000–Rs 14,800.

Q4: Who are the promoters of HDB Financial Services Limited?

HDFC Bank Limited is the promoter of HDB Financial Services Limited. Its stake will reduce from 94.32% pre-issue to 74.19% post-issue.

Q5: What are the main business verticals of HDB Financial Services?

HDB Financial operates across three verticals:

- Enterprise Lending (MSMEs and salaried employees)

- Asset Finance (commercial vehicles, construction equipment)

- Consumer Finance (personal and household loans)

Q6: How are shares reserved for different investor categories?

The total issue of 168,918,919 shares is allocated as follows:

- QIBs: 44.92%

- NIIs: 13.48%

- Retail Investors: 31.44%

- Employees: 0.16%

- Existing HDFC Bank Shareholders: 10.00%

Q7: What are the key financial highlights of HDB Financial Services?

As of 31 March 2025, HDB Financial Services reported total assets of Rs 1,08,663.29 Crore, revenue of Rs 16,300.28 Crore, and Profit After Tax of Rs 2,175.92 Crore, representing a 12% drop from FY24.

Q8: Can HDFC Bank shareholders apply in a special quota?

Yes, HDFC Bank shareholders can apply under a special shareholder quota if they held HDFC Bank shares on or before 19 June 2025.