HDFC Bank stands as a cornerstone of India's financial landscape, playing a pivotal role in both individual and corporate financing. Analysing its loan book, particularly the split between retail and corporate segments, offers crucial insights into the bank's strategic direction, risk appetite, and overall financial health. This article delves into the intricacies of HDFC Bank's lending portfolio, shedding light on its composition, growth, asset quality, and the strategic shifts influencing its future.

Table of Contents

- Defining HDFC Bank's Loan Book: Retail vs. Corporate

- HDFC Bank's Loan Book Composition and Growth Trends

- Asset Quality: A Closer Look at Retail and Corporate Portfolios

- Profitability and Net Interest Margins

- Strategic Focus and Risk Management in Lending

- The Impact of HDFC Ltd. Merger on the Loan Book

- Future Outlook

- Conclusion

- FAQs

HDFC Bank categorises its loans into Retail, Corporate, and Commercial & Rural Banking (CRB) to address diverse customer needs and manage risk effectively.

Retail loans are for individuals (e.g., home, auto, personal), reflecting a growing trend of credit usage. Corporate loans fund businesses for operations or expansion (e.g., term, working capital), offered as secured or unsecured. CRB specifically targets SMEs and agricultural businesses in semi-urban/rural areas, bridging the gap between individual and large corporate clients.

Wrap Up: The strategic segmentation allows HDFC Bank to cater to varied borrower needs, each with distinct risk-reward profiles, underpinning its comprehensive lending strategy and contributing to its overall financial growth.

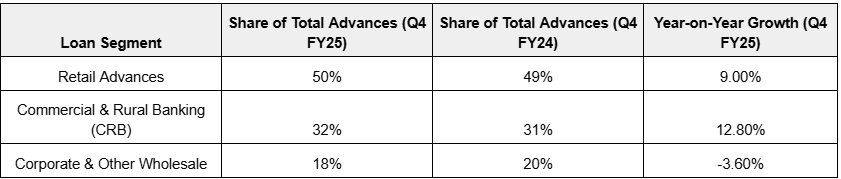

HDFC Bank's loan book composition as of March 31, 2025, reflects its strategic post-merger priorities, emphasising retail and Commercial & Rural Banking (CRB) segments. This deliberate approach influences the bank's growth trajectory and balance sheet management. The bank's total gross advances stood at approximately ₹26.44 lakh crore.

Wrap Up: HDFC Bank's loan book is increasingly geared towards retail and CRB segments, which are currently driving growth. The recent slowdown, especially in corporate loans, is a deliberate post-merger strategy to realign the balance sheet and improve its Credit-to-Deposit ratio. Management anticipates loan growth to align with the system in FY26 and accelerate in FY27.

HDFC Bank continues to demonstrate strong asset quality post-merger, a key indicator of its financial health.As of March 31, 2025, HDFC Bank's Gross Non-Performing Assets (GNPAs) stood at 1.33% and Net Non-Performing Assets (NNPAs) at 0.43%. The bank maintains a healthy provisioning cover of 68% and low credit costs at 0.48% of average advances, supported by strong recoveries.

|

Loan Segment

|

Gross NPA Ratio

(as of March 31, 2025)

|

|

Retail Advances

|

0.79%

|

|

Commercial & Rural Banking (CRB)

|

1.59%

|

|

Corporate & Other Wholesale

|

1.72%

|

Wrap Up: HDFC Bank has maintained solid asset quality even after the merger. Strong recoveries and tight risk control have kept bad loans in check. Provisioning remains healthy, and credit costs are well contained.

Focus on Unsecured Loan Quality

Within retail, unsecured loans (like personal loans) are a key focus. Despite industry stress, HDFC Bank's unsecured retail portfolio remains resilient with a 0.8% GNPA. This is due to a cautious growth strategy that prioritises quality over volume. This careful approach, combined with substantial secured retail loans, underpins the strong asset quality across the entire retail portfolio.

Wrap Up: HDFC Bank maintains robust asset quality, particularly in its retail portfolio. While CRB and corporate segments have slightly higher GNPAs, the bank's prudent provisioning and cautious risk management, especially in unsecured lending, underscore its strong financial health.

Want to dive deeper into the bank’s asset quality metrics? A detailed analysis of HDFC Bank NPA trends and peer comparison offers a clearer picture of credit risk management.

HDFC Bank's profitability is largely driven by its Net Interest Margin (NIM) and substantial fee income, with its dominant retail business playing a crucial role. The post-merger environment has introduced specific dynamics impacting these financial metrics.

- Net Interest Margin (NIM): HDFC Bank's FY25 NIM was ~3.6% up from 3.4% in FY24.

- Return on Assets (RoA): The bank's FY25 RoA was 1.7%, consistently healthy, down from 2.1% in FY24, primarily due to effective credit cost management.

- Fee Income Contribution: Retail fees comprise 94% of total fee income, highlighting the retail franchise's strong profitability. This diversified, high-margin income from payments, cards, and third-party products provides stable revenue.

/content-assets/a2787a3f3d7445e3b46e458c209ce3e8.png)

Wrap Up: despite post-merger NIM pressure, HDFC Bank's profitability is robustly supported by its strong retail business. Strategic emphasis on retail and funding mix optimisation is vital for long-term margin enhancement and resilience.

Want to analyse HDFC Bank's recent stock movement, updated chart patterns, and key valuation metrics? Check the HDFC Bank share price now to evaluate its current market performance.

HDFC Bank's management prioritises a robust strategy for sustainable growth, focusing on loan growth and funding post-merger.

- Emphasis on Credit-to-Deposit (CD) Ratio Reduction: HDFC Bank aims to rapidly reduce its CD ratio (improved to 98% by March 31, 2025). This is achieved by growing deposits significantly faster than loans, prioritising balance sheet optimisation.

- Measured Approach to Loan Growth: The bank adopts a "measured approach" to FY25 loan growth, prioritising profitable, quality growth by re-orienting towards higher-yielding retail and CRB assets to realign its balance sheet.

- Cautious Stance on Unsecured Loans: HDFC Bank deliberately slows unsecured loan growth compared to peers due to internal risk signals. This proactive stance maintains portfolio resilience and asset quality, protecting against high-risk segment downturns.

- Strategic Investments in Distribution and Technology: The bank continues strategic investments in distribution (e.g., semi-urban/rural expansion, IPPB alliance) and technology (digitisation, efficiency) to build infrastructure for long-term, efficient loan origination.

Wrap Up: HDFC Bank's lending strategy emphasises disciplined balance sheet health (CD ratio) and a cautious, strategic approach to loan growth. Proactive risk management and long-term investments position the bank for sustainable, profitable expansion.

The HDFC Bank-HDFC Ltd. merger (July 1, 2023) fundamentally altered the bank's balance sheet, loan book, and funding.

Key Merger Impacts:

- Loan Book & Scale: Merger boosted HDFC Bank's scale, especially in retail mortgages. Net advances reached ₹26.20 lakh crore by March 31, 2025, reflecting post-merger adjustments; pre-merger figures aren't directly comparable.

- Funding & Cost: HDFC Ltd.'s higher-cost liabilities increased HDFC Bank's funding cost to 5.6% (from 3.9% in FY23), pressuring NIMs. The Credit to Deposit ratio peaked at ~110%, requiring a reduction.

- Management Strategy: Management actively integrates synergies, reducing the CD ratio by boosting deposit growth. A key tactic is converting former HDFC Ltd. home loan clients into primary HDFC Bank savings account holders to grow low-cost retail deposits.

Wrap Up: The merger initially raised funding costs and the CD ratio, but HDFC Bank's strategic integration, balance sheet realignment, and aggressive retail deposit growth are key to realising long-term benefits and optimising financial metrics.

HDFC Bank's future outlook focuses on strategic adjustments for sustainable growth and profitability post-merger.

- Loan Growth Trajectory: HDFC Bank anticipates loan growth to align with industry trends in FY26, accelerating in FY27, and prioritising balance sheet optimisation post-merger.

- Funding Mix Improvement: Key efforts are on deepening retail deposit relationships (especially with former HDFC Ltd. clients) to enhance funding mix and restore NIMs, turning a challenge into a long-term advantage.

- Strategic Investments: Continuous investments in digital capabilities and rural/semi-urban expansion will build infrastructure for efficient, long-term growth in high-potential markets.

Wrap Up: HDFC Bank's disciplined strategy—moderating loan growth, aggressively increasing deposits, and cautious unsecured lending—positions it for resilient and sustainable growth. This prioritizes balance sheet strength and risk-adjusted returns for long-term value creation.

There’s a detailed video by Groww that explains how HDFC Bank’s merger with HDFC Ltd has affected its LDR, deposit mobilisation, and cost of funds—worth watching before interpreting recent earnings.

HDFC Bank's loan book analysis reveals a strong strategic shift towards granular, high-yielding retail and Commercial & Rural Banking (CRB) segments, which form 82% of its advances. Post-merger, the bank maintains robust asset quality, especially in retail, and strong non-interest income from retail fees (94% of total). Management's disciplined approach includes aggressive reduction of the CD ratio and cautious unsecured lending, demonstrating a commitment to maintaining balance sheet health.

The bank anticipates moderate loan growth in FY26, followed by acceleration in FY27, with a focus on consolidation. Efforts to deepen retail deposit relationships and continuous investments in digital and rural outreach build long-term, efficient growth. This disciplined and forward-looking strategy positions HDFC Bank for a resilient and sustainable future, prioritising stability and risk-adjusted returns in the evolving Indian banking sector.

Want to compare how HDFC Bank’s retail strategy stacks up against another major private player? Read the full HDFC Bank vs ICICI Bank comparison for a detailed investment perspective.

Q1. What is the composition of HDFC Bank's loan book in 2025?

As of March 31, 2025, HDFC Bank's loan book comprises 50% retail advances, 32% Commercial & Rural Banking (CRB), and 18% corporate and wholesale loans. The bank has strategically shifted towards retail and CRB segments to improve profitability and asset quality.

Q2. How did the HDFC Ltd. merger impact HDFC Bank's loan book?

The merger significantly expanded HDFC Bank’s retail mortgage portfolio and increased its total advances to ₹26.20 lakh crore by March 2025. It also raised the bank’s funding costs and Credit-to-Deposit (CD) ratio, prompting a strategic focus on boosting retail deposits and optimizing loan growth.

Q3. What is the current asset quality of HDFC Bank’s retail and corporate loans?

HDFC Bank maintains strong asset quality with a Gross NPA ratio of 0.80% in retail, 1.89% in CRB, and 1.49% in corporate loans as of March 2025. Its prudent risk management and 68% provisioning coverage protect the portfolio against potential stress.

Q4. Why is HDFC Bank focusing more on retail and CRB lending post-merger?

Retail and CRB loans offer higher yields, better risk-adjusted returns, and diversify the loan book. Post-merger, HDFC Bank prioritizes these segments to balance profitability, improve margins, and manage credit risk while reducing reliance on large corporate lending.

Q5. How is HDFC Bank managing its Credit-to-Deposit (CD) ratio after the merger?

Post-merger, HDFC Bank’s CD ratio peaked at ~110% but was brought down to 96% by March 2025. The bank aggressively mobilized retail deposits, especially by converting former HDFC Ltd. customers to primary depositors, to improve funding mix and financial stability.

Q6. What are HDFC Bank's future plans for loan growth and profitability?

HDFC Bank aims for moderated loan growth in FY26, aligning with market trends, before accelerating in FY27. The strategy includes enhancing retail deposit mobilization, cautious unsecured lending, and investing in digital infrastructure and semi-urban/rural market expansion.