The Indian banking sector is a dynamic landscape, dominated by both established public sector banks and agile private sector players. Among the most prominent are State Bank of India (SBI), the nation's largest public sector bank, and HDFC Bank, a leading private sector giant. This article delves into a comprehensive comparison of these two banking behemoths, examining their financial performance, market presence, customer engagement, and strategic outlook to provide a holistic view.

Table of Contents

- Introduction to SBI and HDFC Bank

- Financial Performance and Key Metrics

- Market Share and Reach

- Customer Base and Satisfaction

- Stock Performance and Investor Sentiment

- Digital Banking and Innovation

- Strategic Focus and Future Outlook

- Conclusion

- Faqs

India's banking system is a unique blend of public and private financial institutions, each playing a crucial role in the nation's economic development. The largest public sector bank and a longstanding institution with a rich history is State Bank of India (SBI). On the other hand, HDFC Bank has become a dominant force in the private sector, known for its effectiveness and customer-focused philosophy.

Wrap Up: These two banks represent distinct models within the Indian banking sector. SBI is a symbol of stability and accessibility, especially in rural and semi-urban regions. On the other hand, HDFC Bank is a prime example of the vibrancy of private banking, which prioritizes reliable performance.

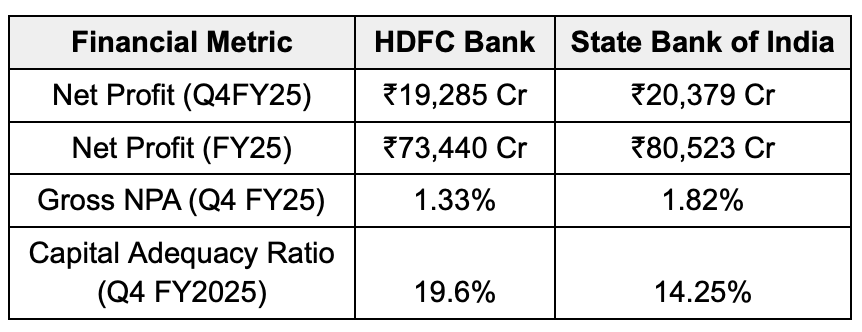

Examining the financial health of HDFC Bank and SBI reveals differing strengths and strategic priorities. While both demonstrate robust financial performance, their approaches to profitability, asset quality, and capital management often vary due to their distinct operational frameworks.

Wrap Up: Overall, HDFC Bank appears stronger in profitability, asset quality, and capital adequacy, while SBI has shown strong recent momentum in profitability and benefits from a larger asset base. Both banks are financially sound and meet RBI's stringent requirements.

To evaluate how HDFC Bank and SBI’s stocks have responded to recent financial performance, check the latest HDFC Bank share price and SBI share price, along with updated charts and valuation indicators.

The market share and geographical reach of HDFC Bank and SBI highlight their differing strategies and target demographics. SBI serves as a cornerstone of financial inclusion across India, whereas HDFC Bank has carved out a presence, particularly in urban and semi-urban centres.

/content-assets/ddb7257097b84d8bb0473e193f5e23a0.png)

Wrap Up: SBI dominates in terms of sheer size, asset base, and customer reach, particularly in the hinterlands, underpinned by its government backing. HDFC Bank, while smaller in comparison, holds a strong market position through its efficiency, higher market capitalisation, and focus on profitable segments.

Understanding customer preferences is crucial for a bank's long-term success. While HDFC Bank and SBI cater to different segments, their customer service and digital offerings shape satisfaction levels. Customers often choose based on digital convenience, branch access, and perceived trustworthiness.

- Customer Base: SBI has a vast rural and urban customer base, while HDFC Bank boasts a loyal, primarily urban clientele.

- Service Quality: HDFC Bank typically offers more personal, faster support, though post-merger feedback varies. SBI's scale can lead to slower, more traditional service.

- Digital Interface: HDFC Bank provides a smooth, intuitive digital experience. SBI's YONO platform is comprehensive but may have occasional glitches.

- Trust & Reliability: SBI's government backing ensures high trust. HDFC Bank earns trust through efficiency and strong financial performance.

Wrap Up: While SBI's vast reach and government backing make it a safe and widely accessible choice, HDFC Bank excels in delivering a superior, tech-driven customer experience, especially for urban clientele. Both banks have a significant number of customers unwilling to switch, highlighting their respective strengths.

Stock performance reflects investor confidence, market dynamics, and the economic climate for HDFC Bank and SBI. These blue-chip stocks often diverge due to unique strengths and perceptions of public versus private banking. Understanding these trends is crucial for investors.

|

Metric

|

HDFC Bank

|

SBI

|

|

1 Year CAGR

|

24%

|

-4%

|

|

3 Year CAGR

|

13%

|

18%

|

|

5 Year CAGR

|

13%

|

33%

|

|

10 Year CAGR

|

14%

|

11%

|

|

Market Cap.

|

15.38 lakh Cr.

|

₹7.23 lakh crore

|

Wrap Up: While HDFC Bank is a long-term favourite for consistent growth, SBI shows stronger short-to-medium term performance. Investors should align choices with their horizons and risk appetites.

Also read how HDFC Bank's FY25 performance has shaped its profitability, provisioning, and dividend payout in the detailed HDFC Bank Q4 FY25 Results.

Digital banking and tech innovation are crucial for banks today. Both HDFC Bank and SBI have heavily invested in digital platforms for seamless service, but their progress reflects their unique structures and priorities.

- Early Adoption: HDFC Bank has consistently led in digital banking, using mobile payments, AI for service, and machine learning for fraud detection.

- Comprehensive Platforms: SBI's YONO platform offers a wide range of integrated banking and lifestyle services.

- Operational Efficiency: Digitalisation has significantly boosted efficiency for both, reducing wait times and branch visits.

- Challenges: HDFC Bank has faced some security and privacy issues. SBI's large size and older systems can slow new tech adoption.

Wrap Up: HDFC Bank leads in digital innovation with a slicker user experience. SBI is rapidly expanding its digital reach, particularly to rural areas, through platforms like YONO. Both are dedicated to digital transformation, but their strategies and execution differ.

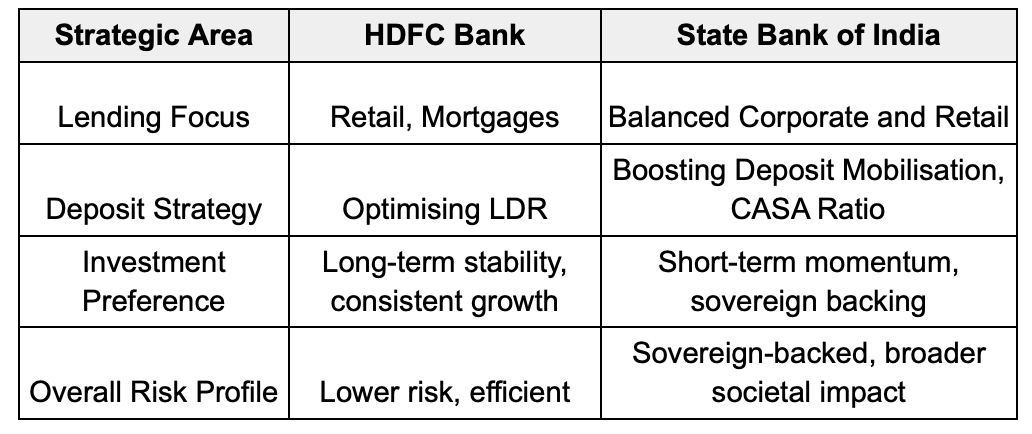

HDFC Bank prioritises profitable growth and digital leadership, while SBI balances its public sector role with commercial viability and financial inclusion. These distinct strategies will shape their future in India's banking sector.

Wrap Up: Both HDFC Bank and SBI are strong players. The choice between them depends on personal preference: HDFC Bank offers profitable growth and digital focus, while SBI provides government backing, extensive reach, and a commitment to inclusion.

There’s a valuable video by CA Rachana Ranade that dissects HDFC Bank’s business, financials, and growth strategy — perfect if you’re comparing it with SBI.

HDFC Bank and SBI are both powerful players in the Indian banking sector, each with unique strengths. HDFC Bank excels in efficiency, digital innovation, and consistent profitability, largely appealing to urban customers. SBI, the largest public sector bank, leverages its vast reach and government backing for financial inclusion and stability, particularly in rural areas.

Choosing between them depends on individual needs: HDFC Bank offers modern, tech-driven banking and strong growth, while SBI provides the assurance of a deeply rooted, government-backed institution. Both remain vital to India's economy, adapting to the evolving financial landscape.

Want to compare how HDFC Bank stacks up against its closest private sector rival? Read this detailed HDFC Bank vs ICICI Bank comparison covering financial strength and growth strategy.

Q1: What are the main differences between HDFC Bank and SBI?

HDFC Bank is a leading private sector bank known for its efficiency, digital innovation, and strong profitability, appealing primarily to urban customers. SBI, the largest public sector bank, is recognized for its vast reach, government backing, and focus on financial inclusion across rural and semi-urban areas.

Q2: Which bank is financially stronger, HDFC Bank or SBI?

While both banks are financially sound and meet RBI requirements, the article indicates that HDFC Bank generally appears stronger in profitability, asset quality (lower Gross NPA), and capital adequacy. However, SBI benefits from a larger asset base and has shown strong recent momentum in profitability.

Q3: Which bank has a larger market share and customer base: HDFC Bank or SBI?

SBI significantly dominates in terms of sheer size, total assets, branch network (over 24,000), and customer reach (over 480 million), particularly in rural India. HDFC Bank, while smaller in comparison, has a strong presence in urban and semi-urban centers with a loyal customer base and higher market capitalization.

Q4: How do HDFC Bank and SBI compare in terms of customer service and digital banking?

HDFC Bank typically offers a more personal, faster service and a smoother, intuitive digital experience. SBI's YONO platform is comprehensive, but its larger scale can sometimes lead to slower, more traditional service and occasional digital glitches. HDFC Bank generally leads in digital innovation with a slicker user experience.

Q5: Which bank offers better stock performance for investors: HDFC Bank or SBI?

In the short to medium term (Year-to-Date 2024 and 1-Year performance), SBI has shown significantly stronger stock performance with a substantial surge. HDFC Bank has seen a decline in the same periods. However, HDFC Bank is often considered a long-term favorite for consistent growth.

Q6: Is SBI or HDFC Bank better for digital banking and innovation?

HDFC Bank has consistently led in digital banking and innovation, offering advanced mobile payments, AI for service, and machine learning for fraud detection. While SBI is rapidly expanding its digital reach, particularly to rural areas via YONO, HDFC Bank generally provides a more polished and efficient digital user experience.

Q7: Which bank is more focused on financial inclusion: HDFC Bank or SBI?

SBI plays a crucial role in financial inclusion across India, with its extensive branch network reaching rural and semi-urban regions, serving as a cornerstone of accessibility for a vast population. HDFC Bank primarily focuses on profitable growth and digital leadership, catering more to urban and growing semi-urban segments.